Prosperity, wealth & the American dream

Redefining the benefits of homeownership

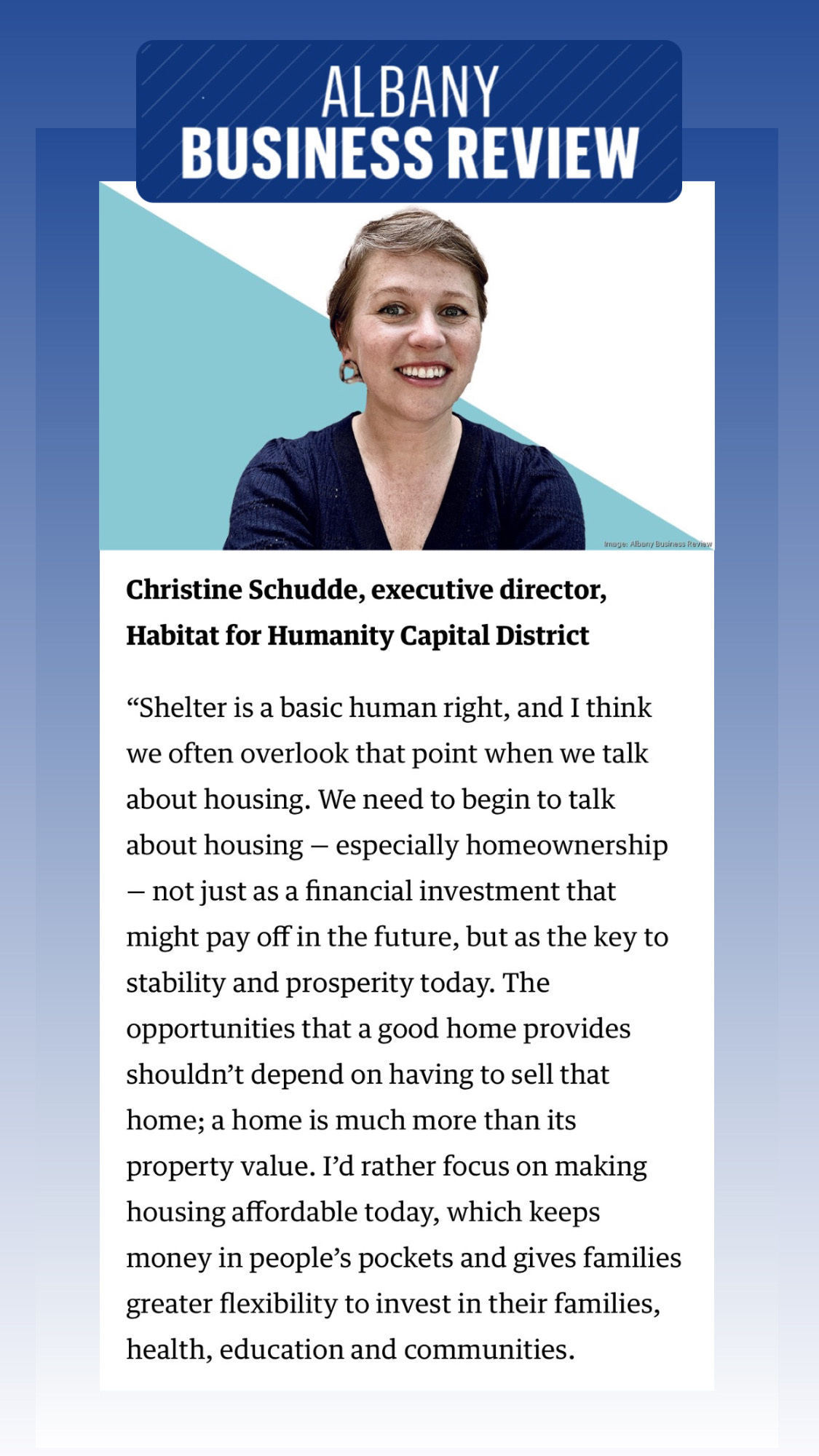

Last month, the Albany Business Review asked a group of local leaders for their thoughts on the unfolding housing crisis in our region.

Here’s what I said:

“Shelter is a basic human right, and I think we often overlook that point when we talk about housing. We need to begin to talk about housing — especially homeownership — not just as a financial investment that might pay off in the future, but as a key to stability and prosperity today.

The opportunities that a good home provides shouldn’t depend on having to sell that home; a home is much more than its property value.

I’d rather focus on making housing affordable [for families] today, which keeps money in people’s pockets and gives families greater flexibility to invest in their families, health, education and communities.

We know that homeownership isn’t a cure-all. We also know that it builds wealth by excluding others from the market. So why do I still believe in its ability to improve people’s lives?

Let’s look at the first line of last week’s report on homeownership from the NY Attorney General’s office:

“Homeownership is deeply tied to prosperity, wealth, and the American dream.”

Prosperity: the condition of being successful or thriving

Having a safe home that you can afford is foundational. The research shows that a good home can improve civic and social engagement, health outcomes, educational achievement and financial stability. The data also point to homeowners achieving better outcomes than renters, including significantly higher net wealth.

So yes, this one checks out. Tenants flourish and prosper too, although we sure make it much more difficult.

Wealth: abundance of valuable material possessions or resources

The dominant rationale behind viewing homeownership as a wealth-building strategy is that if the value of your house increases, you can sell it and cash out.

Of course, this only works if:

You remain a homeowner — you don’t lose your home to foreclosure or disaster.

Your property remains in good repair (true in most markets, although it’s also true that much of your property value comes from the land beneath the home, not the kitchen that you lovingly and expensively renovated and hope will “pay off”).

You sell at the “right time” in the market, which despite what the pundits say is actually hard to predict and it might also not be the right time in your life to sell.

You can then afford something else — houses aren’t like stocks or jewelry, you can’t just cash them out without finding a replacement. So you sell your house for a windfall, but then you have to take that money and find something you can afford in the same high cost market.

You are already wealthy. From 2010 to 2020, almost three-quarters of the increase in property values accumulated to already high-income homeowners.

Instead, I think about equity and wealth in three ways:1

“Pocket equity,” or the monthly savings of having an affordable place to live (the money that stays in their pocket each month)

“Earned equity,” as a result of paying down the mortgage principal each month

“Appreciated equity,” when the home’s value increases over time

Of these three, the one that I’m most interested in, the one that can have the most significant impact on a person’s life, the one that provides more opportunity and freedom and choice… is “pocket equity”.

When you have an affordable place to live, you have options. You can afford life’s basics, you can build your savings, you can help out family members and you can imagine your future, instead of hustling every minute worried about a place to live.

The stability — or even wealth — that an affordable home provides is real. It’s present time. It’s transformational. It builds generational strength while also improving current conditions and financial security. It allows you to put down roots if you want or to move around if you want.

The American dream: tbd

As a country, I think we should dream bigger than just private property ownership.

To start with, we could dream of a society where the stability and protections of homeownership also apply to those who rent their homes. We should advocate for tenant rights and to improve the experience of renting in the United States. After all, homeownership is like rent control for people who can afford a down payment.

Homeownership is at its best when it provides stability and options.

When your home meets the needs of your household, when its affordable to own and maintain, when it becomes a soft landing and sanctuary at the end of a day, when it provides you with safe and quality shelter, when it serves as a foundation in your life. This is the American dream.

The home my parents owned provided stability and security for me throughout my entire childhood, and I’ve seen witnessed how access to affordable homeownership brought hope, stability and financial security for many dozens of Habitat homeowners.

When we expand access to affordable homeownership, families secure their futures. It shouldn’t be the only way to live the American dream — tenants deserve this too — but it’s a road worth traveling.

One more thing

This week the National Association of Realtors reported that the typical homeowner’s net worth grew by $100,000 just since 2019.

Another way to put it, the average house now costs $100,000 more.

The people who saw dramatic increases in their net worth aren’t smarter than those who haven’t. As the expression goes, they were in the right place at the right time — but now others suffer from a worsening affordability crisis. Let’s think bigger and more creatively about homeownership, and how we can reconfigure its responsibilities and benefits!

A big thank you to my colleague Matt Dunbar at Habitat NYC and Westchester County for this framework and the phrase “pocket equity”, which I’ve been borrowing for years, particularly in conversations about the value of “shared equity” homeownership models.

Sp true on many levels, Christine.